82 / 114

82 / 114

[

] 80

Empowering women

through Islamic finance

Kristonia Lockhart, Senior Gender Specialist, Social Capacity

Development Division, Islamic Development Bank

A

t the dawn of the new millennium, the international

community has embarked on a new global agenda.

The many lessons learned over the past 15 years

during the Millennium Development Goals era have been

transformed into an even more ambitious agenda with

aspirations for a more equitable and human-centric develop-

ment. The Sustainable Development Goals (SDGs) adopted

in September 2015 by world leaders have changed the narra-

tive from reducing extreme poverty to ending it, with greater

attention to sustainable development.

To successfully realize the SDGs in a timely manner, certain

prerequisites have to be met. Among the critical issues to be

addressed, financial stability, financial inclusion and shared

prosperity stand out.

The poor are socially excluded; they find themselves voice-

less and powerless. These are key determining factors of

poverty and material deprivation as indicated by their lack of

access to livelihood opportunities. The concept of social exclu-

sion is complex and multifaceted. It refers to individuals and

societies and to disadvantages, alienation and lack of freedom.

It is manifested both formally, through laws and government

institutions, and informally, through community and familial

relations. In poor societies, economic exclusion is at the heart of

the problem. When people are excluded from the main source

of income, their first priority is survival and a basic livelihood.

The size of the financially excluded population is enormous:

according to the United Nations approximately 3 billion people

lack access to formal financial services such as bank accounts,

credit and insurance.

While both men and women face similar barriers to access

finance, evidence suggests that these barriers are higher for

women. Discriminatory social norms and unequal social

and economic structures have led to women and girls being

disproportionately represented among the world’s poor. The

reasons for this include culture, lack of traditional collateral,

women’s lower income levels relative to men, and financial

institutions’ inability to design appropriate products and

outreach strategies to reach women.

Furthermore, in Muslim majority countries there is faith-

compounded financial exclusion. An estimated 72 per cent of

people living in Muslim majority countries do not use formal

financial services even when they are available. Some people view

conventional products as incompatible with the financial prin-

ciples in Islamic law. Islamic finance has gained traction around

the world over the years. It links finance with the real economy

in a substantial way and maintains the link at each point in time

in a fair and transparent manner.

Islamic finance offers promising potential solutions in these

critical domains. In fact, the major financial areas Islamic finance

has contributed to – namely financial stability, financial inclu-

sion and shared prosperity – could be instrumental in ending

poverty, achieving food security, ensuring healthy lives, achiev-

ing gender equality and promoting peaceful and inclusive society.

Additionally, innovative Islamic financial instruments especially

for infrastructure development, such as Sukuk, the Islamic equiv-

alent of bonds, can also be used to mobilize resources to finance

water and sanitation projects, sustainable and affordable energy,

and to build resilient infrastructure and shelter.

The Islamic Development Bank (IDB) Group is a multilateral

institution aiming to promote comprehensive human develop-

ment, with a focus on the priority areas of alleviating poverty,

improving health, promoting education, improving governance

and prospering the people. IDB is striving to promote Islamic

finance, including Islamicmicrofinance, amongmember countries

to enhance financial inclusion and empower low-income families.

IDB has extended Islamic lines of financing for the establish-

ment of Islamic microfinance institutions in member countries

and non-member countries under its Technical Support Program

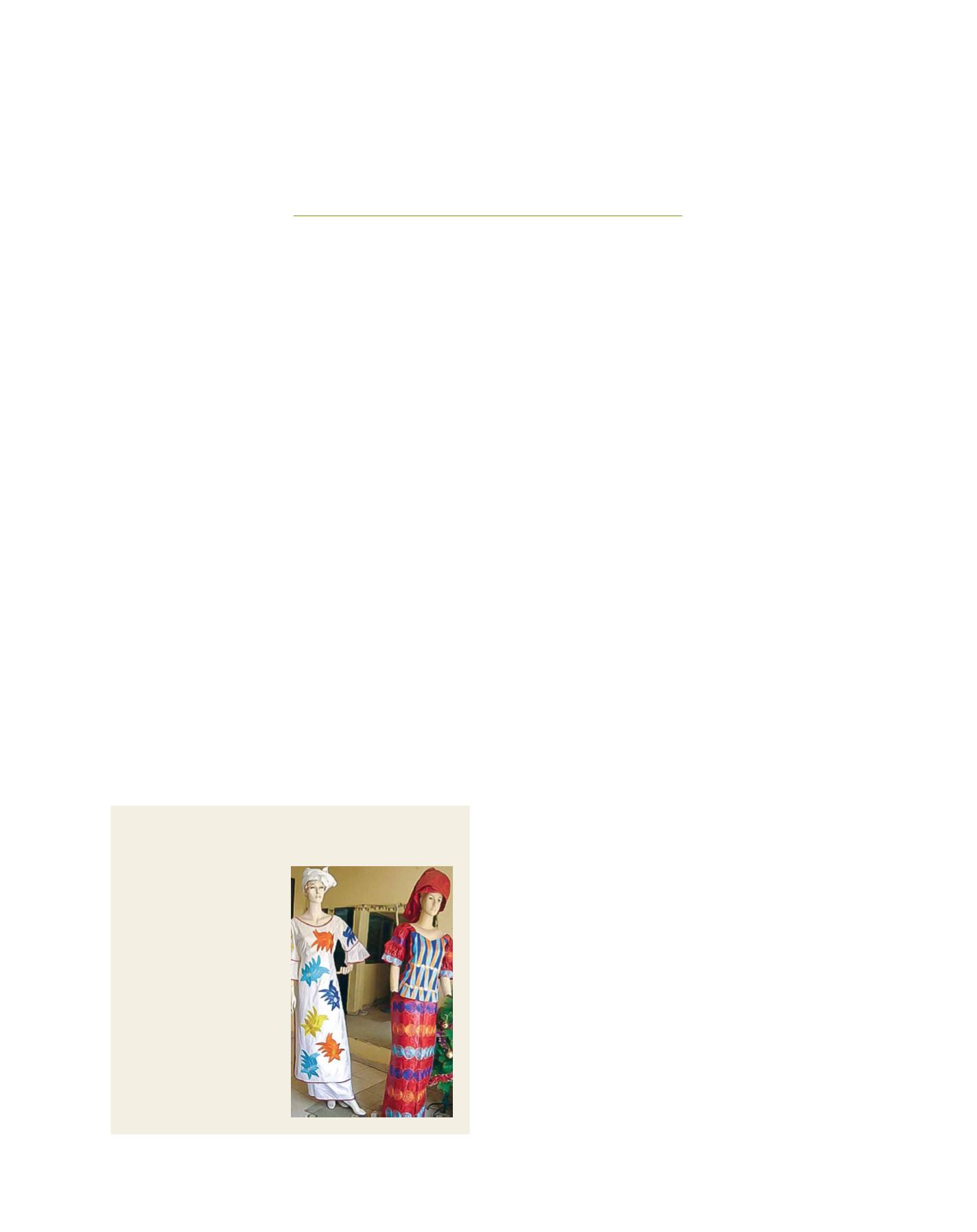

Guinea: producing traditional clothing

A young Guinean woman saw an

opportunity to provide traditional

clothing to the wealthy. She

started her own boutique by

importing fabric and accessories

from France and Germany and

tailor-making garments for

her local clientele. She started

with her own resources and

bought three sewing machines.

As demand grew, she turned

to Crédit Rural de Guinée to

provide financing amounting to

GF30 million, to purchase and

negotiate the price for additional

sewing machines and employ a

few tailors. Today her business

has grown to GF90 million and

she employs 15 people.

Image: IDB

A B

etter

W

orld