69 / 74

69 / 74

[

] 67

J

ust

, P

e aceful

and

I

nclusi v e

S

ocieties

natural resources. The AMV has at its heart the goal to bring

about a “transparent, equitable and optimal exploitation

of mineral resources to underpin broad-based sustain-

able growth and socio-economic development.”

2

The AMV

provides an implementable path for countries to onboard its

fundamental pillars into their approach to mining (see box

on opposite page). Importantly, the AMV represents a para-

digm shift as the only African-owned agenda for mineral use

that puts cooperation, development, linkages and positive

spillover effects above simple extraction and revenue.

As African countries emulate the AMV in their national

policy environment, the consistencies between this and

other development frameworks provide policy makers with

opportunities to streamline their efforts towards mutually

beneficial and reinforcing goals. For example, the many

shared traits between the AMV and the SDGs include: SDG

8 on decent work and economic growth through linkages and

diversification; SDG 9 on industry, innovation and infrastruc-

ture; and SDG 16 on peace, justice and strong institutions to

address mineral governance, Illicit Financial Flows (IFFs)

and rights for local communities. The elements of domes-

tic financial resource mobilization and illicit flows from the

mineral sector inherent in the AMV also overlap with the

mandate of the Addis Ababa Agenda for Action and outcomes

of the Mbeki High Level Panel on IFFs. Indeed, in highlight-

ing the importance of responsible, nationally-owned and

inclusive use of natural resources to spur transformation,

the AMV served as a precursor to many of these frameworks.

AMV progress realized with coordination from the

African Minerals Development Centre

The African Minerals Development Centre (AMDC) was

established in 2013 as custodian of the AMV, in order to

assist African member states with implementation and

mainstreaming in national frameworks. AMDC support is

demand-driven based on requests and needs of member states

and thus takes many forms in response to context specifici-

ties. This can include technical support, capacity building,

assistance with political and governance aspects of the AMV,

and other areas. This variety of flexible support in adopting

the AMV is coordinated as a comprehensive Country Mining

Vision (CMV) for each country with which the AMDC

engages. AMDC operates along a structure of seven work-

streams, directly relating to the pillars of the AMV, and has

worked in over half of all AU member States. AMDC support

is resulting in practical implementation of the AMV and, by

extension, progress towards the SDGs in a number of specific

initiatives, a snapshot of which are detailed here:

Identifying opportunities for economic linkages, value addition and

regional value chains

While the need for mineral-based industrialization is well

acknowledged, the specific means to build this requires

thorough empirical analysis and recognition of the politi-

cal economy of the sector, country and region in question.

Indeed, a delicate coordination is needed of all the activi-

ties that will foster such linkages, including infrastructure

investments, skilling of labour, agglomeration of producers

through economic clusters, facilitation of business connec-

tions and incentivizing of production and investment flows,

amongst others. In recognition of this, AMDC is increasingly

providing analysis and identification of linkage and produc-

tion potential as a part of its CMV guidance. One example of

this is support to Ghana to establish a supplier development

programme which will identify upstream inputs that can be

produced domestically to service both the well-established

mining sector and other established and rising industries,

and the investments needed to enable local suppliers to

produce these. Given the scale and history of gold extrac-

tion in Ghana, and the mostly untapped potential in bauxite,

manganese and iron ore, AMDC is advocating a transfor-

mation of the vicious cycle wherein mining activities yield

raw exports and consume manufactured imports into a

virtuous circle of mineral outputs being harnessed for use

in construction, industry, metal working and other activi-

ties, the outputs of which can then serve as local inputs into

domestic and regional mining. Regarding this regional lens,

ongoing consultations with the government are also address-

ing the role of regional integration and trade in linking with

neighbouring markets throughout ECOWAS. Indeed, domes-

tic demand for and production of such items may be too small

to incentivize investments and reach efficient economies of

scale, but pooling national markets can allow for this critical

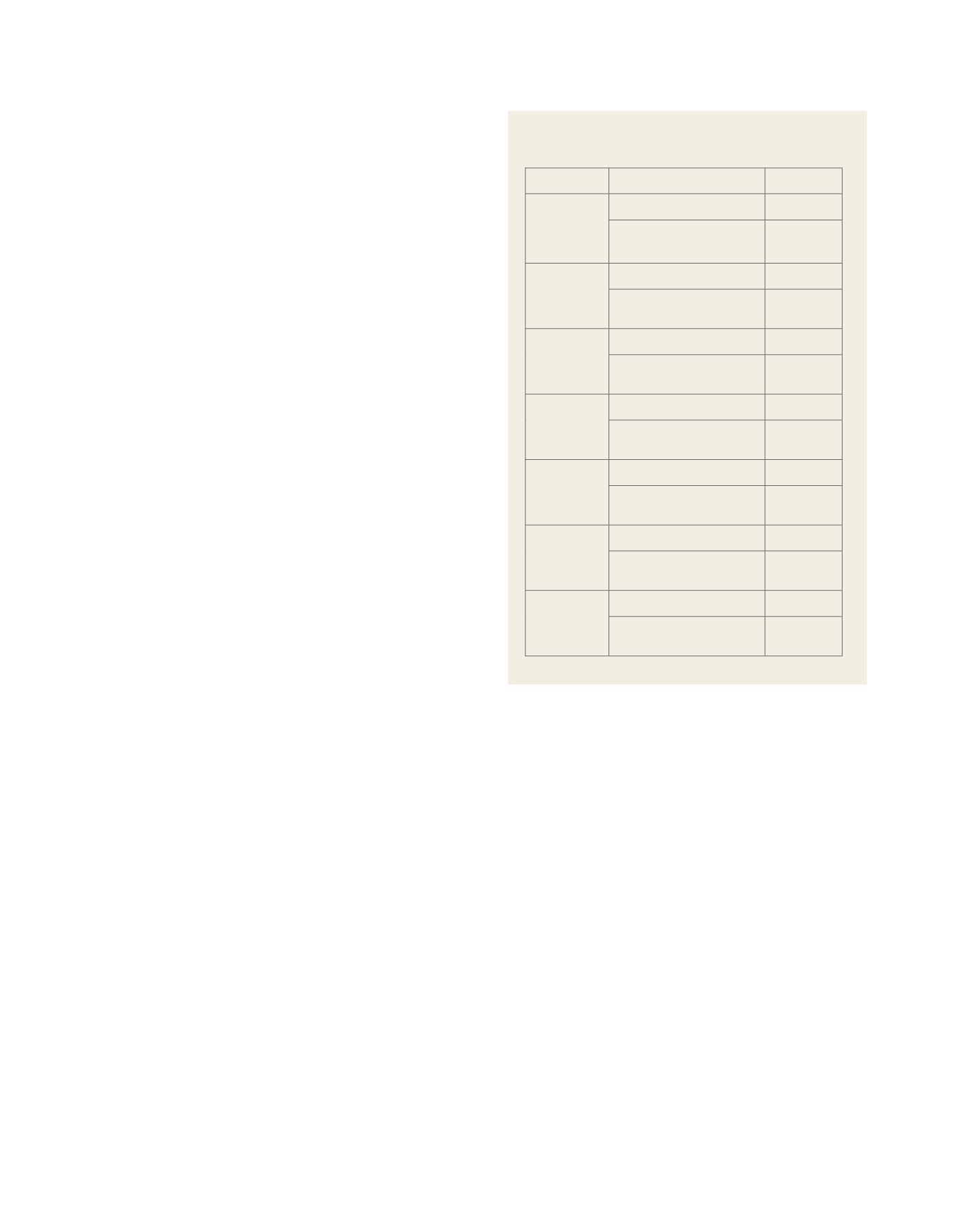

Minerals as a percentage of GDP and exports,

select African countries

Country

Series

2014 value

Madagascar

Mineral rents (% of GDP)

3.51

Ores and metals exports (%

of merchandise exports)

36.82

Mauritania

Mineral rents (% of GDP)

27.58

Ores and metals exports (%

of merchandise exports)

59.51

Morocco

Mineral rents (% of GDP)

1.92

Ores and metals exports (%

of merchandise exports)

7.88

Mozambique Mineral rents (% of GDP)

0.03

Ores and metals exports (%

of merchandise exports)

34.43

Tanzania

Mineral rents (% of GDP)

2.39

Ores and metals exports (%

of merchandise exports)

17.36

Zambia

Mineral rents (% of GDP)

12.81

Ores and metals exports (%

of merchandise exports)

78.16

Zimbabwe

Mineral rents (% of GDP)

3.83

Ores and metals exports (%

of merchandise exports)

24.5

Source: Authors’ Calculations based on World Bank WDI 2017